Manager Review: Lawrence Burns

Lawrence Burns – Deputy manager, Scottish Mortgage

- The third era of generative artificial intelligence has arrived, with agents now able to plan, use tools and complete complex tasks with less human prompting.

- AI agents are reshaping software and challenging traditional pricing models, while increasing demand for the infrastructure AI depends on.

- Scottish Mortgage is focused on the exceptional companies positioned to benefit as AI becomes cheaper, more capable and more widely deployed across the economy.

As with any investment, your capital is at risk.

Agentic Dawn

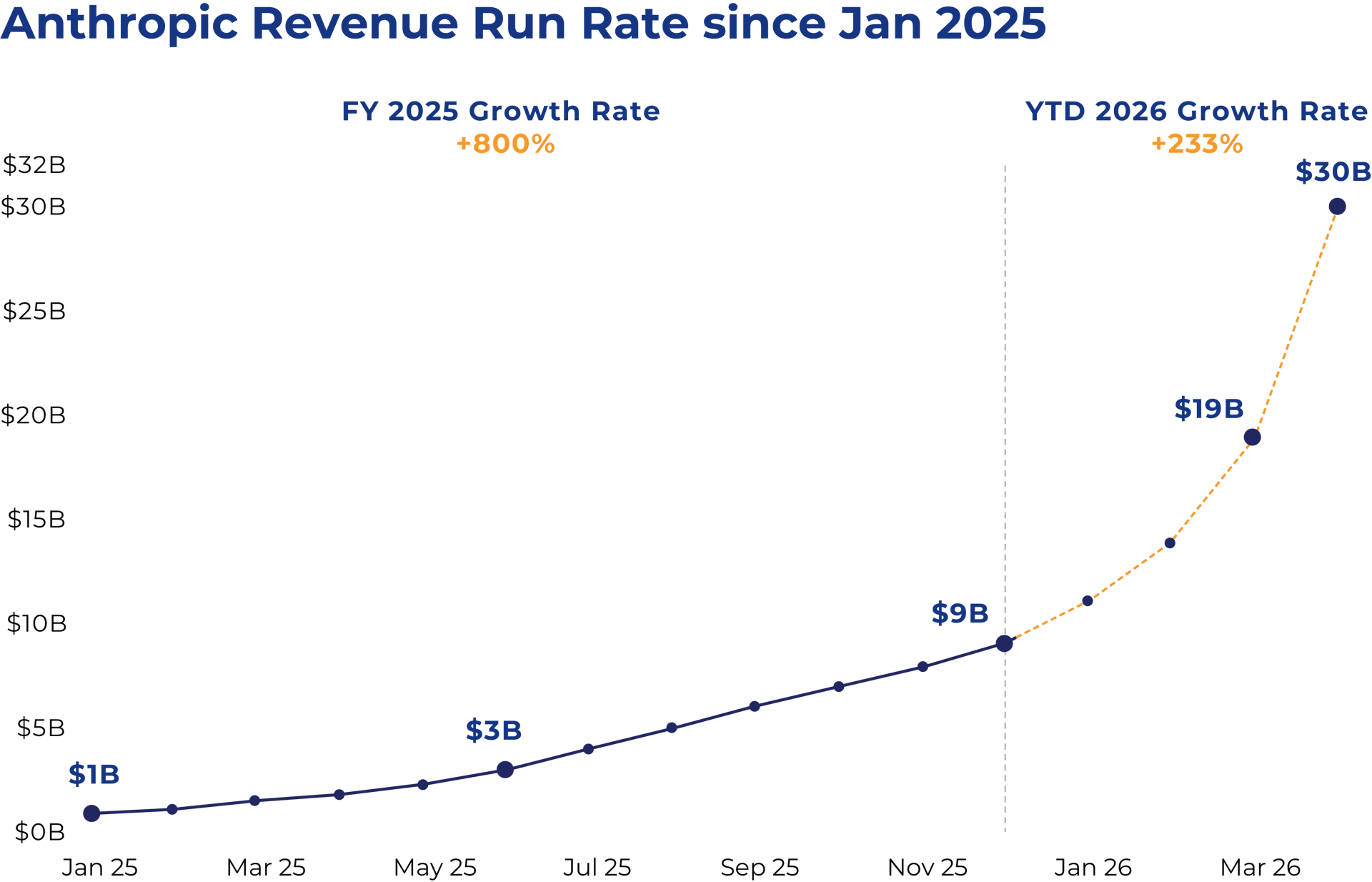

In January 2025, the artificial intelligence company Anthropic had an annualised revenue run rate of $1bn – a measure that takes recent sales and projects them over a full year. Fifteen months later, it had surpassed $30bn. No company in recorded history has grown organic revenue at this scale and pace.

Anthropic, one of Scottish Mortgage’s private holdings, has helped usher in the third era of generative artificial intelligence. The first was the conversational era, which began with the launch of OpenAI’s ChatGPT in late 2022, when models became reliably capable of following natural-language instructions and holding back-and-forth exchanges with their users.

The second was the reasoning era, which began with OpenAI’s o1 in September 2024, when models learned to pause, think through problems step by step and produce considered, rather than instinctive, answers. This made them better at solving complex problems, particularly in mathematics, science and coding.

By late November 2025, with the release of Anthropic’s Claude Opus 4.5, the agentic era had become unmistakable. Models could now be given a goal and work towards it over many steps: planning, using tools, checking their work and producing useful outputs without constant human prompting. Each era has built on the last rather than replaced it. Today’s agents are reasoning models that have learned to act, just as reasoning models were conversational models that had learned to think.

The implications of the rise of agents reach across our portfolio into the structure of the software industry, the value of consumer businesses, the rise of a parallel Chinese AI ecosystem, and the physical supply chain that must be built to meet insatiable computational demands.

Software

The impact of agents has been felt first at scale in software. There the work is digital, the value is high, the goals are often clear, and feedback comes quickly.

If an application is not working properly, an agent can be asked to find the problem, write a fix and test the result before users receive the update.

Adoption has been rapid. Google’s chief executive has said that 75 percent of new code is now written by AI. The founder of one of our portfolio companies recently told us that it is spending more on AI coding tools for its engineers than it is paying them in compensation. Moreover, he claimed the company gets a better return on the tools than on the engineers themselves. At Anthropic itself, AI is now writing between 70 and 90 percent of all code.

We are heading towards a future in which software is increasingly built, operated and used by agents. This has profound implications. First, it weakens the link between software value and the number of ‘seats’ – licensed users within an organisation – on which much of the sector’s pricing rests. Second, it lowers the barriers to creating software, raising competitive intensity and eroding moats built on accumulated code and complexity. Third, it raises a deeper question about where value will accrue for each company: whether it’s to the software applications themselves or to the intelligence layer that understands the task, draws on the relevant data, and directs the work.

The market has reacted quickly. The global software sector has lost roughly $2tn in market capitalisation over the past 12 months. Some repricing is likely justified: starting valuations left little room for the questions now being asked about pricing power, competition and value capture. But the repricing has also been indiscriminate. Not all software is equal. In particular, there is a difference between software that is primarily a product for humans to use, and software that provides the infrastructure on which other digital activity depends. The former may be more exposed if agents change how people interact with applications. The latter may benefit as agents generate more demand for the rails beneath them: data queries, security checks, compute workloads, payments and identity.

The impact of agents will not remain confined to software development.

Our own software holdings are skewed towards this infrastructure layer. Databricks and Snowflake organise the governed company data that agents need if they are to be useful inside enterprises. Cloudflare provides the network and security layer on which agent applications can run, while helping websites identify, control and charge AI agents for access. Adyen and Stripe provide the payment and trust infrastructure that allows agents to transact safely on behalf of customers and merchants. Stripe’s founders have been careful not to overstate the speed of change, arguing that agentic commerce is likely to arrive in small chunks rather than one sudden leap; but each chunk of autonomy still requires programmable, permissioned and trusted financial rails.

Far beyond software development

The impact of agents will not remain confined to software development. Most knowledge work, when stripped down to its components, is some combination of reading, writing, reasoning and using software as a tool to get things done. These are precisely the capabilities at which agents are now becoming proficient. Work that has long looked specialised: drafting a legal memo; synthesising a clinical trial; building a financial model; reviewing a patent application, is specialised at the level of expertise but generic at the level of cognitive operation. The consequence is that agents are not a tool for one industry but many.

The same logic applies to consumer businesses. Agents will become our personal shoppers, financial advisors and everyday assistants. This creates risk if horizontal AI assistants sit between customers and platforms. But the strongest platforms control assets an agent needs: trust, customer history, payments, credit, logistics, product catalogues and merchant networks. Amazon, MercadoLibre and Sea Limited are thus looking to build their own vertical agents to serve their platforms and enable shopping beyond them as well.

Nubank offers a similar possibility in finance. Long before agents were in vogue, its founder, David Vélez, told us that Nubank’s ambition was to give every customer a private banker in their pocket. Agents could make that ambition more practical: helping users manage bills, understand spending, choose when to borrow, build savings and find the cheapest rates on the market. Agents improve price transparency, tailor options to personal circumstances and reduce the friction to taking action. For Vélez, this is an opportunity. As a low-cost operator, Nubank is well placed to seize it.

Few companies will be left untouched by these developments. For some, agents will create new demand; for others, they will threaten existing profit pools; for many, they will do both at once. This will be a key challenge of growth investing in the years ahead. Scottish Mortgage is well placed to meet it because we invest across both public and private markets. Many of the companies shaping the AI frontier remain private, and our access to them gives us a broader view of how quickly the technology is improving, how it is being adopted, and where value may ultimately accrue.

Beyond the Valley

Meeting that challenge also requires geographic perspective. It is tempting to read the AI story as a Silicon Valley one. On questions of frontier model capability, that reading is broadly right. But it is incomplete. China is not merely a follower in artificial intelligence. It is developing different strengths under different conditions.

The first is physical AI. Simulation will be vital, but embodied intelligence improves fastest when virtual training is connected to real-world deployment. China’s manufacturing base matters because it provides the world’s largest deployment surface. This is reinforced by the largest installed stock of industrial robots, dense local supply chains, supportive policy, and an electric vehicle industry already combining software, hardware and cost-focused manufacturing. Horizon Robotics, one of our holdings, sits directly in this intersection between AI and the physical world, enabling autonomous cars with the ambition to extend this into broader robotics.

The second is cost-performance. Restricted access to the most advanced chips has pushed Chinese model companies to do more with less. This matters because the agentic era will be far more compute-intensive than the conversational era. If agents are to be widely adopted, the cost of useful intelligence must fall dramatically. MiniMax, one of our holdings, develops open-source models that approach frontier capability at a fraction of the training cost, part of a wider Chinese ecosystem pushing intelligence down the cost curve. Low-cost models do not need to win every benchmark to matter. They can win by making intelligence cheap enough to embed into software agents, consumer apps, enterprise workflows, robots and cars.

Our holding in ByteDance points to a third Chinese strength: productisation. The ByteDance AI bot Doubao shows how quickly generative AI can become a mass consumer habit when attached to a company that understands recommendation, interface design and viral distribution. It leads the Chinese market with more than 226 million monthly active users. The next phase of AI will not be shaped only by those with the largest models. It will also be shaped by those that can make intelligence cheap, useful, physical and habitual.

Physical supply chain

These changes all come with immediate implications for the physical supply chain. Each successive era of generative artificial intelligence has added a new layer of compute demand without removing the last. Model training was the original enabler of the conversational era and continues to scale as frontier labs build ever-larger models. The reasoning era added a second layer. Models no longer simply produced an answer; they spent more computing power working through problems, checking their logic and considering alternatives before responding.

The agentic era has added a third layer of compute demand and it’s the fastest-growing. Anthropic’s data shows that a single agent consumes four times the computational work of a chat conversation, and a multi-agent system around 15 times. The bigger change, however, is that until now, demand for AI was implicitly capped by human attention. A person could only ask so many questions in a day, and each answer had to wait for the next prompt. Agents have effectively removed that cap. Given a goal, an agent loops through the reasoning process dozens of times, runs autonomously even while humans sleep, and increasingly works with other agents in coordination on the same task.

If AI disrupts most industries, then avoiding it doesn't remove risk; it merely shifts it.

The three eras present compounding S-curves of compute demand, with none yet plateauing and each steeper than the last. The consequence is a sharp and continuing rise in demand for chips. It is this logic that underpins our holdings across the chip supply chain in TSMC and ASML, which are among our largest positions, and NVIDIA, to which we have been adding.

Investing in the supply chain is, in effect, a bet on the growth of AI itself, rather than a bet on which company will capture it. Whichever applications succeed and whichever frontier models prevail, the underlying compute demand runs through the same handful of companies. This is what makes investing in the supply chain such an unusually attractive way to own the growth of AI.

The pattern of revolutions

We are well aware that the history of revolutionary technology is also a history of market overshoot. Human and market psychology have a reliable capacity to misprice the path of even the most transformational innovation. The railway companies of the nineteenth century reshaped the modern economy. At their 1880s peak, they comprised roughly 60 percent of the entire US stock market, before a series of busts wiped out a great deal of capital. The canal buildout of the late eighteenth century and the fibre-optic buildout of the late 1990s followed a similar pattern: real technological progress, real economic impact, and real financial excess. We should expect the AI buildout to echo that history.

Yet the rational response is not to stand aside from a technological revolution. That is not the safe position it may appear to be. If AI disrupts most industries, then avoiding it doesn’t remove risk, it merely shifts it. You might still own businesses exposed to disruption, and not own the businesses in line for generational upside.

The harder task is to remain invested without becoming indiscriminate: to distinguish between durable value and temporary exuberance, between enabling infrastructure and fragile applications, and between companies that merely invoke AI and those that can turn it into enduring economic advantage.

The emergence of capable agents has made us more convinced that AI demand can keep expanding. But history argues for humility. There will be waste, disappointment and overbuilding along the way. Our job is not to believe every claim made for AI, but to own the exceptional companies that can benefit as intelligence becomes cheaper, more capable and more widely deployed.

Scottish Mortgage

Annual past performance to 31 March each year (%)

|

|

2022 |

2023 |

2024 |

2025 |

2026 |

|

Share Price |

-9.5 | -33.5 | 32.5 | 6.0 | 26.8 |

|

NAV* |

-13.1 | -17.8 | 11.5 | 11.2 | 27.4 |

|

Benchmark** |

12.8 | -0.9 | 21.0 | 5.5 | 18.0 |

Performance figures appear in GBP, total return. NAV is calculated with borrowings deducted at fair value. *NAV = Net Asset Value. **FTSE All World Index (GBP) TR. Performance source: Morningstar and FTSE.

Past performance is not a guide to future returns.

Legal notice

Source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2025. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" "Russell®", is/are a trade mark(s) of the relevant LSE Group companies and is/are used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

Unlisted investments such as private companies, in which the Trust has a significant investment, can increase risk. These assets may be more difficult to sell, so changes in their prices may be greater.

About the author - Lawrence Burns

Deputy manager, Scottish Mortgage

Lawrence Burns was appointed deputy manager of Scottish Mortgage in 2021. He joined Baillie Gifford in 2009 and became a partner of the firm in 2020. During his time at the firm, his investment interest has become focused on transformative growth companies. He has been a member of the International Growth Portfolio Construction Group since October 2012 and in 2020 became a manager of Vanguard’s International Growth Fund. Lawrence is also co-manager of the International Concentrated Growth and Global Outliers strategies. Prior to this, he also worked in both the Emerging Markets and UK Equity teams. Lawrence graduated BA in Geography from the University of Cambridge in 2009.

Regulatory Information

This content was produced and approved at the time stated and may not have been updated subsequently. It represents views held at the time of production and may not reflect current thinking. Read our Legal and regulatory information for further details.

A Key Information Document is available by visiting our Documents page. Any images used in this communication are for illustrative purposes only.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). The investment trusts managed by Baillie Gifford & Co Limited are listed on the London Stock Exchange and are not authorised or regulated by the FCA.

Baillie Gifford Overseas Limited (BGO) provides investment management and advisory services to non-UK clients. BGO is wholly owned by Baillie Gifford & Co. Both are authorised and regulated in the UK by the Financial Conduct Authority.

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 (BGA) holds a Type 1 licence from the Securities and Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes and closed-ended funds such as investment trusts to professional investors in Hong Kong.

Baillie Gifford Asia (Singapore) Private Limited (BGAS) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence to conduct fund management activities for institutional investors and accredited investors in Singapore. BGA and BGAS are wholly owned subsidiaries of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Scottish Mortgage Investment Trust PLC (the “Company”) is an alternative investment fund for the purpose of Directive 2011/61/EU (the “AIFM Directive”). Baillie Gifford & Co Limited is the alternative investment fund manager (“AIFM”) of the Company and has been authorised for marketing to Professional Investors in this jurisdiction.

This communication is made available by Baillie Gifford Investment Management (Europe) Limited (“BGE”), which has been engaged by the AIFM to carry out promotional activities relating to the Company. BGE is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform promotional, advisory and Individual Portfolio Management activities. BGE has passported its authorisations under the mechanisms set out in the AIFM Directive.

Australia

This information is provided to you on the basis that you are a “wholesale client” within the meaning of section 761G of the Corporations Act 2001 (Cth) (“Corporations Act”). In no circumstances should this information be made available to a “retail client” within the meaning of section 761G of the Corporations Act. This information contains general information only. It does not take into account any person’s objectives, financial situation or needs.

Belgium

The Company has not been and will not be registered with the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten / Autorité des services et marchés financiers) (the FSMA) as a public foreign alternative collective investment scheme under Article 259 of the Belgian Law of 19 April 2014 on alternative collective investment institutions and their managers (the Law of 19 April 2014). The shares in the Company will be marketed in Belgium to professional investors within the meaning the Law of 19 April 2014 only. Any offering material relating to the offering has not been, and will not be, approved by the FSMA pursuant to the Belgian laws and regulations applicable to the public offering of securities. Accordingly, this offering as well as any documents and materials relating to the offering may not be advertised, offered or distributed in any other way, directly or indirectly, to any other person located and/or resident in Belgium other than to professional investors within the meaning the Law of 19 April 2014 and in circumstances which do not constitute an offer to the public pursuant to the Law of 19 April 2014. The shares offered by the Company shall not, whether directly or indirectly, be marketed, offered, sold, transferred or delivered in Belgium to any individual or legal entity other than to professional investors within the meaning the Law of 19 April 2014 or than to investors having a minimum investment of at least EUR 250,000 per investor.

Germany

The Trust has not offered or placed and will not offer or place or sell, directly or indirectly, units/shares to retail investors or semi-professional investors in Germany, i.e. investors which do not qualify as professional investors as defined in sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB) and has not distributed and will not distribute or cause to be distributed to such retail or semi-professional investor in Germany, this document or any other offering material relating to the units/shares of the Trust and that such offers, placements, sales and distributions have been and will be made in Germany only to professional investors within the meaning of sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB).

Luxembourg

Units/shares/interests of the Trust may only be offered or sold in the Grand Duchy of Luxembourg (Luxembourg) to professional investors within the meaning of Luxembourg act by the act of 12 July 2013 on alternative investment fund managers (the AIFM Act). This communication does not constitute an offer, an invitation or a solicitation for any investment or subscription for the units/shares/interests of the Trust by retail investors in Luxembourg. Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units/shares/interests of the Trust to retail investors in Luxembourg.

Switzerland

The Trust has not been approved by the Swiss Financial Market Supervisory Authority (“FINMA”) for offering to non-qualified investors pursuant to Art. 120 para. 1 of the Swiss Federal Act on Collective Investment Schemes of 23 June 2006, as amended (“CISA”). Accordingly, the interests in the Trust may only be offered or advertised, and this document may only be made available, in Switzerland to qualified investors within the meaning of CISA. Investors in the Trust do not benefit from the specific investor protection provided by CISA and the supervision by the FINMA in connection with the approval for offering.

Singapore

This communication has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, this communication and any other content or material in connection with the offer or sale, or invitation for subscription or purchase, of the Trust may not be circulated or distributed, nor may be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor (as defined in Section 4A of the Securities and Futures Act 2001, as modified or amended from time to time (SFA)) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1), or any person pursuant to Section 275(1A), and in accordance with the conditions specified in Section 275 of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where the Trust is subscribed or purchased under Section 275 by a relevant person which is:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the securities pursuant to an offer made under Section 275 except:

(1) to an institutional investor or to a relevant person or to any person arising from an offer referred to in Section 275(1A) or Section 276(4)(c)(ii) of the SFA,

(2) where no consideration is or will be given for the transfer;

(3) where the transfer is by operation of law; or

(4) pursuant to Section 276(7) of the SFA or Regulation 37A of the Securities and Futures (Offers of Investments) (Securities and Securities-based Derivatives Contracts) Regulations 2018.