Scottish Mortgage forum: why we continue to back innovation

Stewart Heggie – Commercial Director

Key Points

- A recent forum updated investors on performance, disruptive opportunities and private companies

- The Trust’s managers highlighted the need for companies to be adaptable and resilient to shocks

- They also stressed the importance of patience – which can hopefully lead to extraordinary rewards

As with any investment, your capital is at risk

Investment drives change, and change drives long-term returns. That’s the core belief that guides Scottish Mortgage’s managers on their hunt for exceptional growth companies, with the aim of investing in them for five years or longer.

The Trust’s managers Tom Slater and Lawrence Burns have stuck to this approach in the face of recent unfavourable market conditions. They have done so because they believe that only by embracing discomfort can they generate outsized returns.

The managers updated shareholders at a forum in London in June.

Reflections

Slater opened by reflecting on performance. He remarked on the fact that recent interest rate rises and the invasion of Ukraine, among other factors, had hit confidence in parts of the economy and led some companies to cut costs. This has been reflected in the Trust’s own share price.

“We are disappointed with the outcome we’ve delivered for shareholders over the past year,” Slater said.

“However, we hope you don’t own Scottish Mortgage on the basis of the outcome in any one year.”

A long history

Asset value of Scottish Mortgage Investment Trust since 1910

Slater added that one of the first questions he and Burns ask, is whether the business would be resilient to external shocks and could adapt to changing conditions. And he said that the recent challenges were “predominantly transient in nature”, only rarely affecting the case for staying invested in the Trust’s portfolio companies.

Disruption opportunities

Slater explained that technological progress continued to march forward.

Disrupting industries

Innovation does not come from the ‘experts’

| Looking back | Looking ahead |

| Retail innovation It wasn’t Walmart… It was Amazon (ecommerce) |

Healthcare innovation Maybe it’s not J&J, GSK or Novartis… Maybe it’s Moderna? |

|

Media innovation |

Logistics innovation Maybe it’s not FedEx or UPS… Maybe it’s Zipline? |

| Automotive innovation It wasn’t GM/Ford/VW… It was Tesla |

Food innovation Maybe it’s not Nestle or Tyson… Maybe it’s Upside Foods? |

| Space innovation It wasn’t Boeing or Lockhead Martin… It was SpaceX |

Can you think of a major innovation in the last 4O years that has come from so called ‘experts’? |

Developments in fields as diverse as semiconductors, advanced software, genomic sequencing and cloud computing are opening up new opportunities.

He highlighted a few areas of particular excitement:

Healthcare

Scottish Mortgage’s largest holding, Moderna, became a household name thanks to its Covid-19 vaccine. It now has 30 vaccines for infectious diseases in clinical trials, as well as a personalised cancer vaccine, in the pipeline. Recent trials on advanced melanoma showed a 44 per cent increase in survival compared to the current standard of care. Meanwhile, firms such as Tempus Labs and Recursion are also developing new treatments using artificial intelligence (AI) techniques.

The energy transition

The long-term trend towards electrification continues. The US has legislated for significant investment to remain competitive with Chinese companies attempting to dominate related supply chains. Batteries will be critical – Slater quoted statistics from McKinsey predicting that the battery market would equal 4.7 terawatt-hours (TWh) in size by 2030, compared with 700 gigawatt-hours (GWh) in 2022. For comparison’s sake, that would be enough to power more than 67 million homes for a year. Firms such as the US battery recycler Redwood Materials, the electrical aircraft venture Joby Aviation and the European battery manufacturer Northvolt stand to gain. The latter has announced $55bn of contracts with car manufacturers and is scaling rapidly to meet industry needs.

Artificial intelligence

There have been several meaningful breakthroughs over the past year, most noteworthy the success of ChatGPT. AI will transform many parts of the economy. As Slater noted: “Ten years ago, Marc Andreessen characterised the investment approach of his venture capital firm with the idea that software is eating the world... The way I look at it, at this point, AI is starting to eat software.” He explained that most companies are having board-level discussions about how to inject generative AI – the ability for software to create text, images and computer code at similar levels to humans – into their business models. This is a huge opportunity for NVIDIA, the leading provider of computer chips used to train AI models, and ASML, the only firm making machines capable of manufacturing the most advanced chips.

Why private companies?

Over the last decade, private company investing has become a core part of the Scottish Mortgage approach.

Size

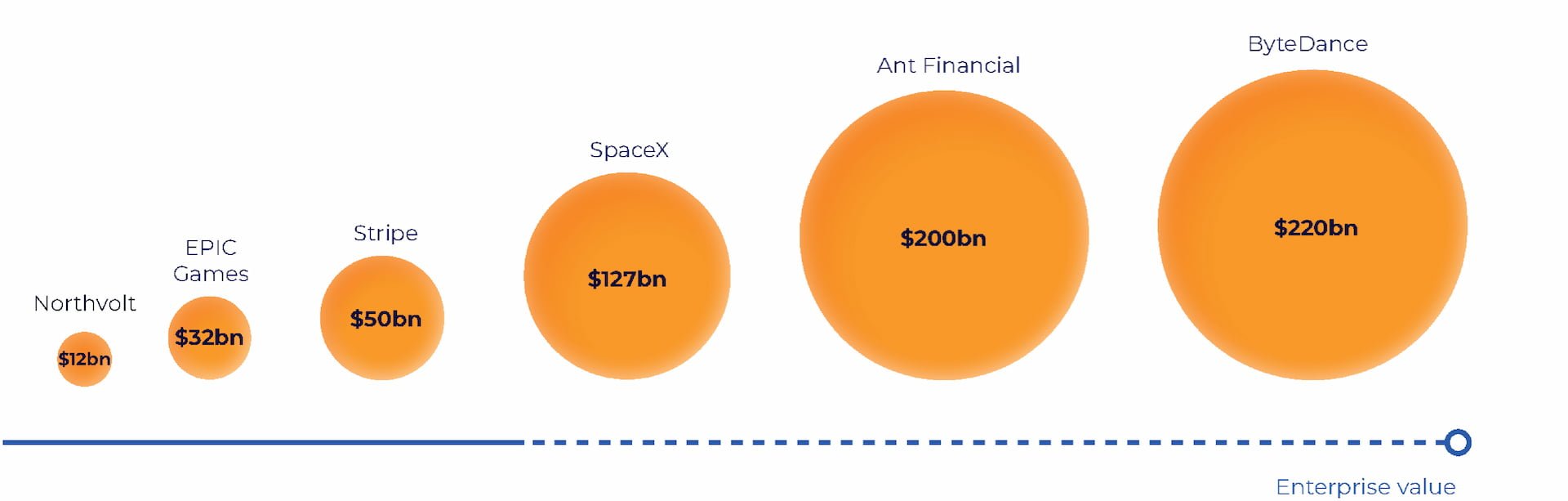

Private companies in Scottish Mortgage top 30 with enterprise values over $10bn

Private companies give the Trust ‘s shareholders a chance to own exceptional businesses at a rapid growth stage, many of which have no public market equivalent. Burns outlined four further reasons to take stakes in them:

- Companies are staying private for longer. As Burns explained, “We have a number of companies that are valued at more than $100bn and have been private for quite a long time… Often we agree with [the decision to stay private], as there are a lot of drawbacks to being a public company. The companies that make up the bulk of our private exposure, therefore, are neither small nor early-stage.”

- Scottish Mortgage’s scale, structure and reputation as a patient shareholder give it an edge, which attracts the attention of private companies. “This matters,” Burns said, “because the most sought-after private companies have a long list of people that want to invest in them, and they’re able to choose who their investors are.”

- “Understanding how the world is changing solely through public companies is akin to trying to construct a puzzle with half the pieces missing,” Burns said. “I remember going to the Bay Area in 2018 and meeting startup after startup hoping to disrupt their industry by building the next big AI chip. It was that process and having access to those private companies that gave us more conviction in terms of NVIDIA’s edge.”

- Traditionally, investing in world-leading private companies has been neither accessible nor cheap. Even leading venture capital funds can find it difficult to get access, and the fees they charge their own investors are typically high. By contrast, Scottish Mortgage democratises access while taking pride in keeping its fees low.

What’s on shareholders’ minds?

As always, the forum gave attendees the opportunity to ask questions.

Burns answered one about finding private companies by explaining that three common ways involve:

- the managers scouting for potential investments by travelling to China, Latin America and India, among other regions

- founders and other private company leaders contacting Scottish Mortgage

- being recommended by existing partners – including portfolio company executives and venture capital firms Scottish Mortgage has previously invested alongside

Slater responded to a question about Elon Musk’s recent behaviour. He remarked that ordinary people rarely change the world, and that Tesla and SpaceX’s recent execution has been phenomenal. He added that while Musk often comes up with visionary ideas, he is surrounded by highly capable managers who execute them with proven operational expertise.

Slater was also quizzed about when he last “pressed the button” to buy Scottish Mortgage shares. He revealed that he had done so three weeks previously.

It’s the plainest example of the fact that, despite uncertainty over what’s happening in the market, the managers have conviction in their investments.

And Burns highlighted another important quality. “To hold the next big winners takes patience,” he said. “What we try to do is own companies where if you're patient, the reward for being so is hopefully extraordinary.”

Scottish Mortgage Annual Past Performance To 31 March each year (net %)

| 2019 | 2020 | 2021 | 2022 | 2023 |

| 16.5 | 12.7 | 99.0 | -9.5 | -33.6 |

Source: Morningstar, share price, total return, sterling.

Past performance is not a guide to future returns.

The trust invests in overseas securities. Changes in the rates of exchange may also cause the value of your investment (and any income it may pay) to go down or up.

The trust invests in emerging markets where difficulties in dealing, settlement and custody could arise, resulting in a negative impact on the value of your investment.

The trust has a significant investment in private companies. The trust’s risk could be increased as these assets may be more difficult to sell, so changes in their prices may be greater.

About the author - Stewart Heggie

Commercial Director

Stewart Heggie is a commercial director, focused on serving the needs of Scottish Mortgage shareholders. Prior to joining in 2019, he spent 15 years as a discretionary fund manager, before which he helped design the investment platform of a large UK bank. Nowadays, Stewart enjoys a varied role that spans across several areas involved in running a listed investment company. He plays a key role in developing the company’s strategic direction and broadening out its ownership. Beyond that, he works closely with the managers to maintain current portfolio knowledge; regularly meets with potential and existing overseas shareholders; and acts as a key contact for the board of directors.

Regulatory Information

This content was produced and approved at the time stated and may not have been updated subsequently. It represents views held at the time of production and may not reflect current thinking. Read our Legal and regulatory information for further details.

A Key Information Document is available by visiting our Documents page. Any images used in this content are for illustrative purposes only.

This content does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). The investment trusts managed by Baillie Gifford & Co Limited are listed on the London Stock Exchange and are not authorised or regulated by the FCA.

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 (BGA) holds a Type 1 licence from the Securities and Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes and closed-ended funds such as investment trusts to professional investors in Hong Kong.

Baillie Gifford Asia (Singapore) Private Limited (BGAS) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence to conduct fund management activities for institutional investors and accredited investors in Singapore. BGA and BGAS are wholly owned subsidiaries of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Europe

Scottish Mortgage Investment Trust PLC (the “Company”) is an alternative investment fund for the purpose of Directive 2011/61/EU (the “AIFM Directive”). Baillie Gifford & Co Limited is the alternative investment fund manager (“AIFM”) of the Company and has been authorised for marketing to Professional Investors in this jurisdiction.

This content is made available by Baillie Gifford Investment Management (Europe) Limited (“BGE”), which has been engaged by the AIFM to carry out promotional activities relating to the Company. BGE is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform promotional, advisory and Individual Portfolio Management activities. BGE has passported its authorisations under the mechanisms set out in the AIFM Directive.

Belgium

The Company has not been and will not be registered with the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten / Autorité des services et marchés financiers) (the FSMA) as a public foreign alternative collective investment scheme under Article 259 of the Belgian Law of 19 April 2014 on alternative collective investment institutions and their managers (the Law of 19 April 2014). The shares in the Company will be marketed in Belgium to professional investors within the meaning the Law of 19 April 2014 only. Any offering material relating to the offering has not been, and will not be, approved by the FSMA pursuant to the Belgian laws and regulations applicable to the public offering of securities. Accordingly, this offering as well as any documents and materials relating to the offering may not be advertised, offered or distributed in any other way, directly or indirectly, to any other person located and/or resident in Belgium other than to professional investors within the meaning the Law of 19 April 2014 and in circumstances which do not constitute an offer to the public pursuant to the Law of 19 April 2014. The shares offered by the Company shall not, whether directly or indirectly, be marketed, offered, sold, transferred or delivered in Belgium to any individual or legal entity other than to professional investors within the meaning the Law of 19 April 2014 or than to investors having a minimum investment of at least EUR 250,000 per investor.

Germany

The Trust has not offered or placed and will not offer or place or sell, directly or indirectly, units/shares to retail investors or semi-professional investors in Germany, i.e. investors which do not qualify as professional investors as defined in sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB) and has not distributed and will not distribute or cause to be distributed to such retail or semi-professional investor in Germany, this document or any other offering material relating to the units/shares of the Trust and that such offers, placements, sales and distributions have been and will be made in Germany only to professional investors within the meaning of sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB).

Luxembourg

Units/shares/interests of the Trust may only be offered or sold in the Grand Duchy of Luxembourg (Luxembourg) to professional investors within the meaning of Luxembourg act by the act of 12 July 2013 on alternative investment fund managers (the AIFM Act). This document does not constitute an offer, an invitation or a solicitation for any investment or subscription for the units/shares/interests of the Trust by retail investors in Luxembourg. Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units/shares/interests of the Trust to retail investors in Luxembourg.

Switzerland

The Trust has not been approved by the Swiss Financial Market Supervisory Authority (“FINMA”) for offering to non-qualified investors pursuant to Art. 120 para. 1 of the Swiss Federal Act on Collective Investment Schemes of 23 June 2006, as amended (“CISA”). Accordingly, the interests in the Trust may only be offered or advertised, and this document may only be made available, in Switzerland to qualified investors within the meaning of CISA. Investors in the Trust do not benefit from the specific investor protection provided by CISA and the supervision by the FINMA in connection with the approval for offering.

Singapore

This content has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, this content and any other content or material in connection with the offer or sale, or invitation for subscription or purchase, of the Trust may not be circulated or distributed, nor may be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor (as defined in Section 4A of the Securities and Futures Act 2001, as modified or amended from time to time (SFA)) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1), or any person pursuant to Section 275(1A), and in accordance with the conditions specified in Section 275 of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where the Trust is subscribed or purchased under Section 275 by a relevant person which is:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the securities pursuant to an offer made under Section 275 except:

(1) to an institutional investor or to a relevant person or to any person arising from an offer referred to in Section 275(1A) or Section 276(4)(c)(ii) of the SFA,

(2) where no consideration is or will be given for the transfer;

(3) where the transfer is by operation of law; or

(4) pursuant to Section 276(7) of the SFA or Regulation 37A of the Securities and Futures (Offers of Investments) (Securities and Securities-based Derivatives Contracts) Regulations 2018.