The atmospheric rise of cloud computing

Claire Shaw – Portfolio Director

Key Points

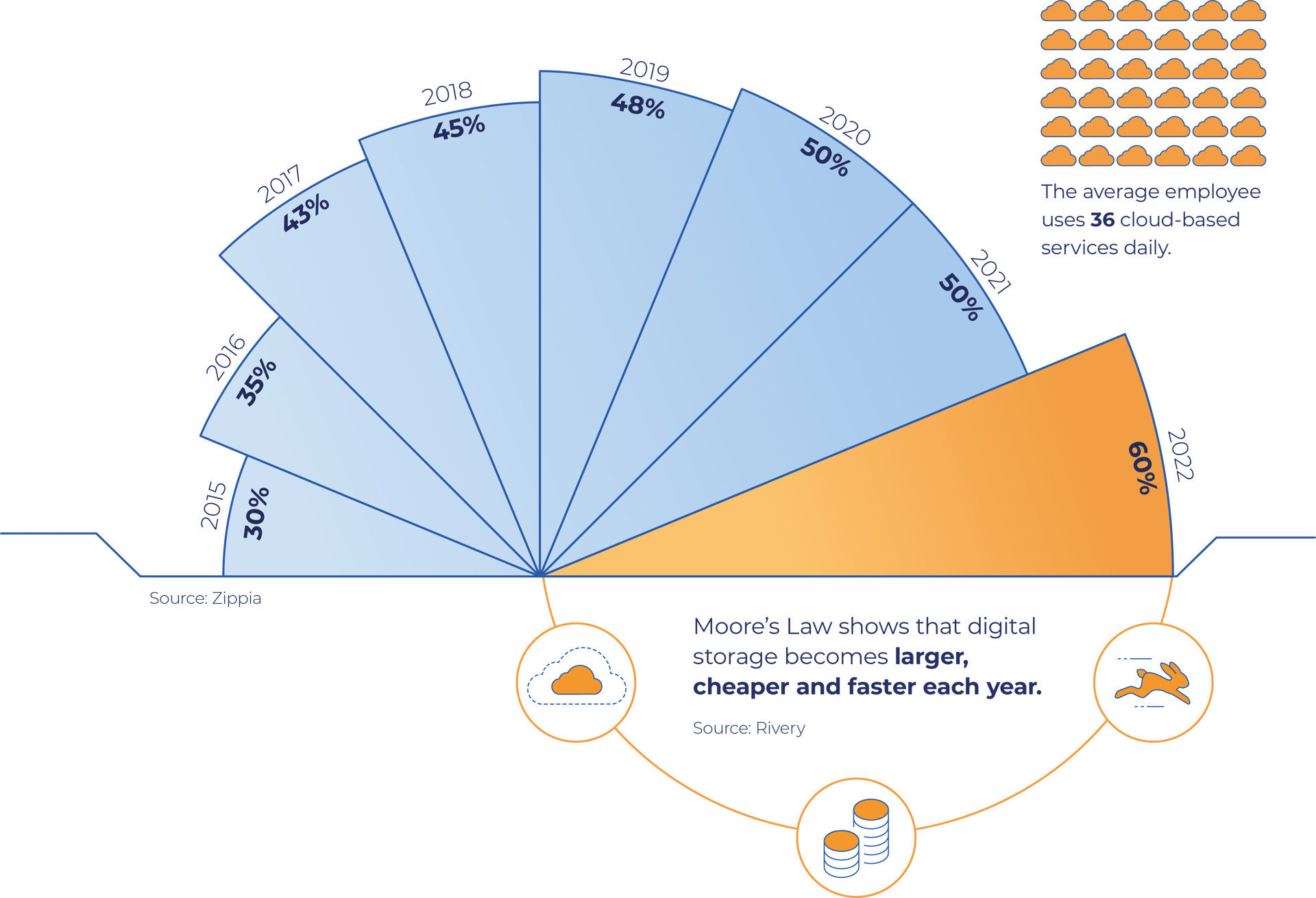

- By 2025, 200 zettabytes of data – the equivalent to the storage capacity of 755 billion 256GB iPhones – will be stored in the cloud

- Snowflake’s data warehouses allow customers to gather their data in one place and Databrick’s data lake helps scientists to use machine learning to analyse data

- By 2026, 45 per cent of information technology spending could be allocated to innovative cloud development and management firms

As with any investment, your capital is at risk.

From the dawn of civilisation to 2003, five exabytes of stored information has been created. Today, this much is created every two days.

Also, the world will generate more data in the next three years than in the last 30. And by 2025, half of it (200 zettabytes) will be on the cloud.

Sources: Forbes, Cybersecurity Ventures

What does the cloud hold?

Many types of data, from word files, images and videos to large archives and applications data are stored on the cloud. And more than 90 per cent of the world’s corporations use it to store 60 per cent of their data, a 100 per cent increase from 2015.

Sources: Spiceworks and Zippia

Yearly growth of corporate data stored in the cloud

Types of cloud services

There are different types of cloud storage systems according to the end-users and their needs.

Storage types

![]()

Private

Suitable for large enterprises

![]()

Hybrid (private and public)

Suitable for small and mid-sized companies

![]()

Public

Suitable for individual users and mid-size companies

![]()

Community (multiple companies’ shared private storage)

Suitable for financial, health, legal and compliance companies

All these types of cloud services require physical infrastructure, mostly in the form of data warehouses and data lakes.

Scottish Mortgage holdings Snowflake and Databricks are two companies at the forefront of this industry.

Sources: DataBricks, Snowflake, IBM and Contrary Research

Data warehouse

![]()

A centralised repository that collects data from various sources and organises it into a single format.

![]()

Data is transformed, cleansed, and integrated before being loaded into the warehouse.

![]()

It is structured and optimised for fast and efficient querying and analysis, making it a good choice for Business Intelligence (BI) and data-driven decision-making.

![]()

Snowflake hosts a data warehouse that allows customers to gather all their data into one place and gain useful business insights. It is built on the foundation of a data warehouse.

Data lake

![]()

A massive, scalable repository that stores raw, unstructured data in its original format.

![]()

Data is stored in its rawest form and is processed later when accessed for various purposes.

![]()

It is optimised for handling batch processing and is ideal for data scientists and engineers who need raw data to work with.

![]()

Databricks hosts a data lake which is primarily used for storing data but its main aim is to help data scientists use machine learning tools to analyse the data.

There is a third type, data lakehouses. Combining the processing power of data warehouses and the storage size of data lakes, they increase flexibility and responsiveness in analysing data, allowing organisations to make faster and more informed business decisions. They are also more cost-effective.

Sources: Data Warehousing Fundamentals, Snowflake

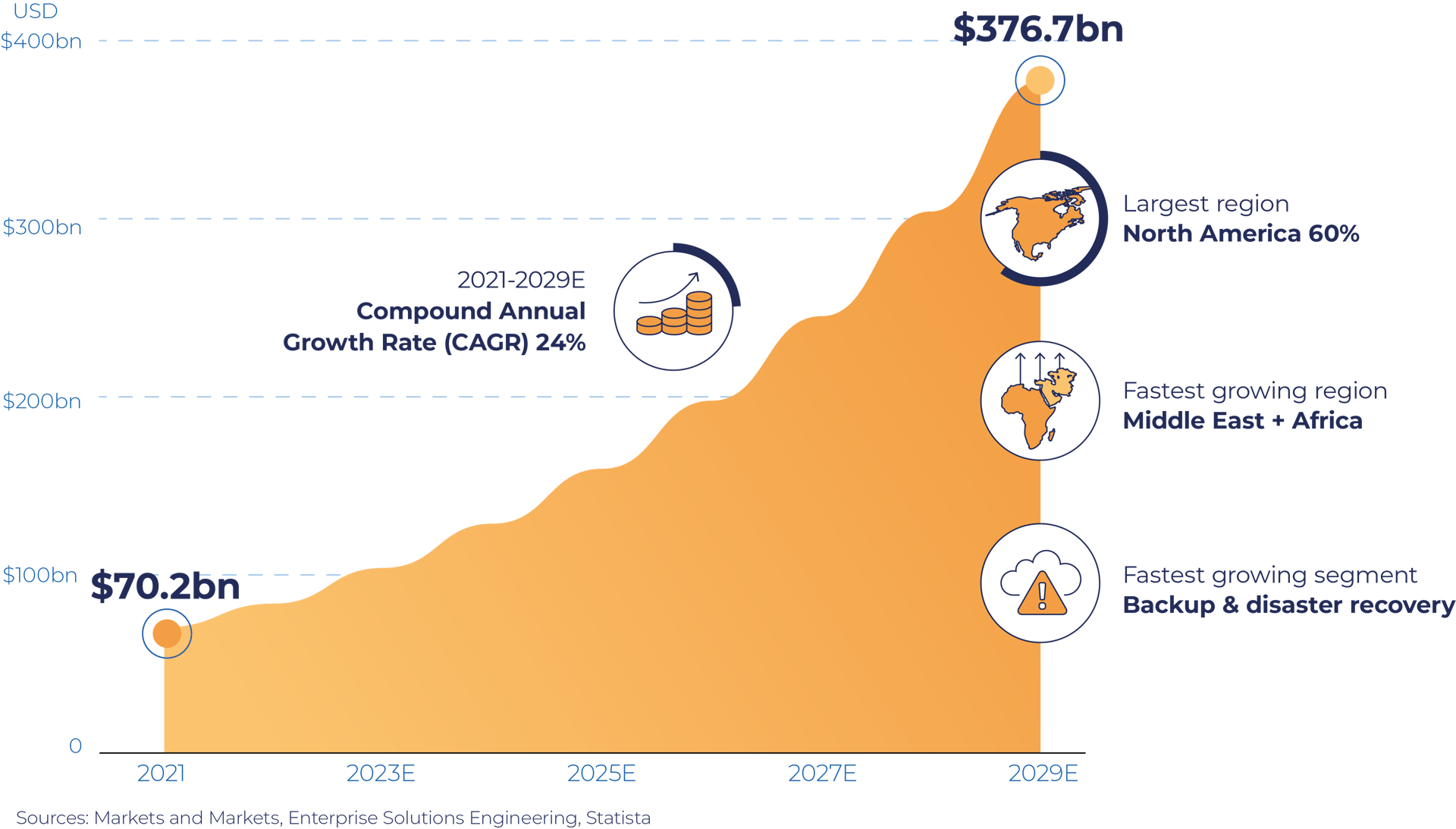

Market value and projections

Overall, the storage segment of the market is expected to continue its upwards trajectory in the coming years.

Global cloud storage market 2021-2029E

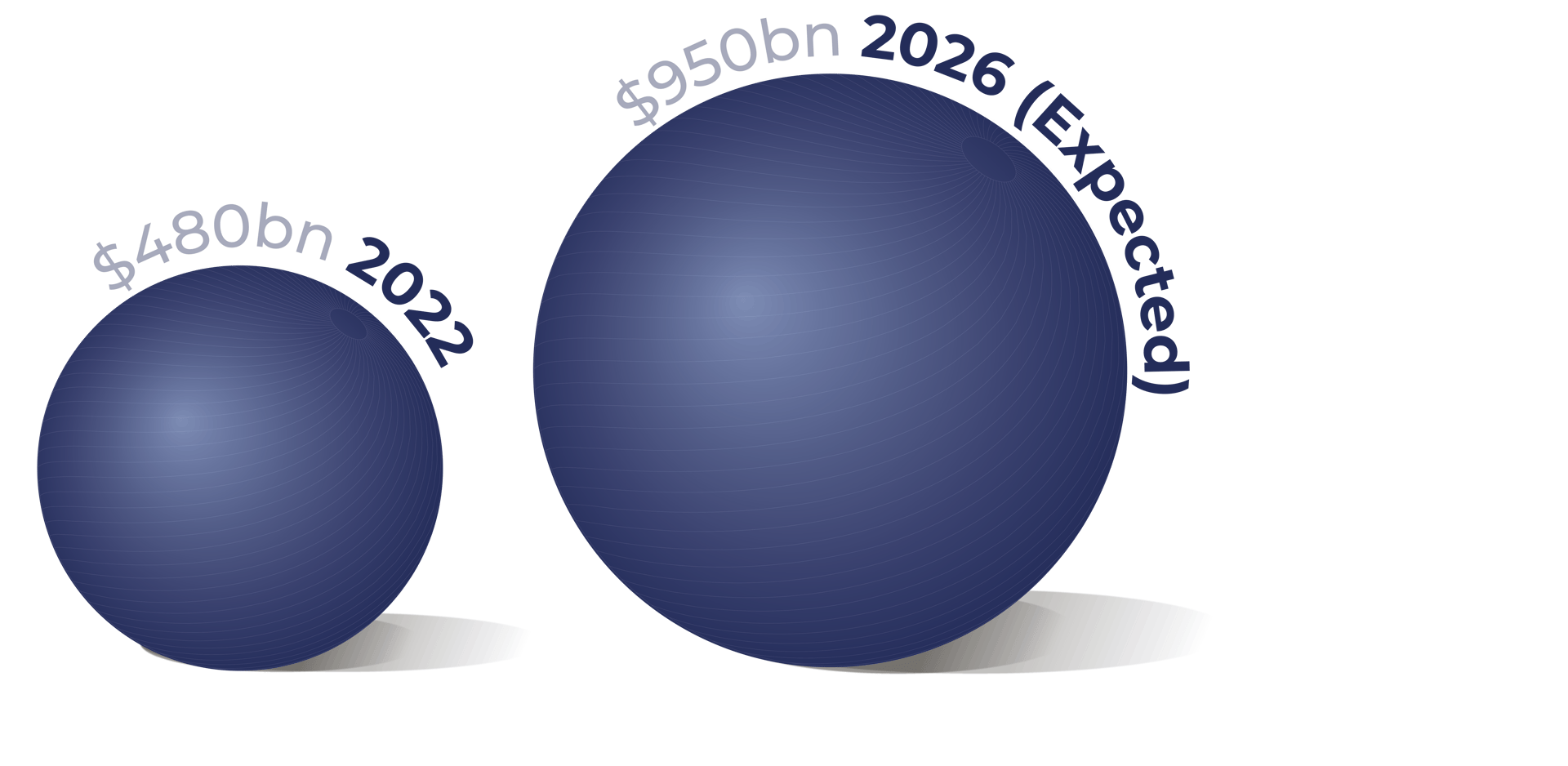

Apart from storage services, cloud computing is expected to be worth $950bn by 2026—almost twice what it was in 2022.

Source: Zippia

But how are they different?

Cloud storage v cloud computing

Cloud storage

Data storage capacity made available over the cloud, eg Google Drive, Microsoft OneDrive and Dropbox.

Cloud computing

Processing power made available over the cloud to do computational tasks, eg Microsoft Azure, Amazon Web Services and Google Cloud.

Source: computertech.com

It is anticipated that by 2026, 45 per cent of all IT spending will be allocated towards innovative cloud development and management firms, such as Snowflake, which provides access to near-limitless data reserves, and Databricks, which is leading the way in lakehouse technology for comprehensive storage solutions.

Sources: Gartner, Snowflake, Databricks

Investing in such modern cloud systems will be key to driving progress and innovation for the future.

The atmospheric rise of cloud computing

From the dawn of civilisation right up until 2003, human beings generated five exabytes of stored information. Now this is created every two days.

And by 2025, half of all the world’s data will be found on the cloud, allowing people to save, control and work with it remotely or in any other setting.

In the infographic above, sponsored by Scottish Mortgage Investment Trust, we dive into everything you need to know about the atmospheric rise of cloud computing.

What does the cloud hold?

Many types of data, from text files, images and videos to large archives and applications data, are stored on the cloud.

Today, the average employee uses 36 cloud-based services daily, and corporations as a whole store about 60 per cent of their data on the cloud.

Different cloud storage services have been created based on this growing demand. Consequently, there are four main cloud storage systems according to Spiceworks:

- Private cloud storage: The data and resources in a private cloud are not typically shared with other organisations or users. This is suitable for large enterprises.

- Public cloud storage: Available to the public and is managed by a third-party provider. The resources and data in a public cloud is shared among multiple users and organisations.

- Hybrid cloud storage: Combines both private and public cloud infrastructure. This allows organisations to use the public cloud for non-sensitive data and the private cloud for sensitive data. This is therefore more suitable for small and mid-sized companies.

Community cloud storage: Shared among organisations with similar goals, policies and security requirements. The organisations or a third-party provider can manage the community cloud. It is suitable for financial, health, legal, compliance systems, etc.

Types of cloud storage infrastructure

Cloud storage systems require physical infrastructure, and the primary types are:

- Data warehouses are storage houses that collect data from various sources and organise it into a single format. They allow fast information processing and analysis. This makes them a good choice for business intelligence (BI) and data-driven work.

- Data lakes store raw data in their original format. They efficiently handle batch processing and are ideal for data scientists and engineers working with raw data.

- Data lakehouses offer the combined services of warehouses and lakes.

Individuals and organisations can increase flexibility and responsiveness when analysing data by using data warehouses’ processing power and data lakes’ storage size, both of which are becoming larger and more powerful each year.

Current market value and future projections

Despite the global cloud storage market being just one segment of the overall cloud computing market, it is expected to reach over $376bn with a compound annual growth rate (CAGR) of 24 per cent.

|

Year |

Global Market Value ($bn) |

|

2021 |

$70.2bn |

|

2022 |

$87.0bn |

|

2023 |

$107.9bn |

|

2024 |

$133.8bn |

|

2025 |

$165.3bn |

|

2026 |

$203.6bn |

|

2027 |

$250.4bn |

|

2028 |

$307.5bn |

The fastest-growing regions for the cloud storage market are the Middle East and Africa. Moreover, the fastest-growing segment is backup and disaster recovery.

The fast expansion of cloud computing as a whole is expected to catapult the market to a staggering $947.3bn by 2026—almost double what it was in 2022.

Cloud storage versus cloud computing

Cloud computing and cloud storage are often used interchangeably but are not the same. Cloud computing provides processing power made available over the cloud to do computational tasks, eg Amazon Web Services and Google Cloud.

However, cloud storage provides data storage capacity available over the cloud, eg Google Drive, Microsoft OneDrive and Dropbox.

By 2026, 45 per cent of all information technology (IT) spending is anticipated to be allocated toward innovative cloud development and management firms.

Investing in the cloud

Investing in companies such as Databricks and those providing modern cloud systems, such as Snowflake, will be key to driving progress and innovation in the future.

About the author - Claire Shaw

Portfolio Director

Claire Shaw is a portfolio director and plays a prominent role in servicing Scottish Mortgage’s UK shareholder base. Before joining in 2019, she spent over a decade as a fund manager with a focus on managing European equity portfolios for a global client base. With a background in analysing companies and communicating investment ideas, Claire is also responsible for creating engaging content that makes the Scottish Mortgage portfolio accessible to all its shareholders. Beyond that, she works closely with the managers, meeting with portfolio companies and conducting in-depth portfolio discussions with shareholders.

Regulatory Information

This content was produced and approved at the time stated and may not have been updated subsequently. It represents views held at the time of production and may not reflect current thinking. Read our Legal and regulatory information for further details.

A Key Information Document is available by visiting our Documents page. Any images used in this content are for illustrative purposes only.

This content does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). The investment trusts managed by Baillie Gifford & Co Limited are listed on the London Stock Exchange and are not authorised or regulated by the FCA.

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 (BGA) holds a Type 1 licence from the Securities and Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes and closed-ended funds such as investment trusts to professional investors in Hong Kong.

Baillie Gifford Asia (Singapore) Private Limited (BGAS) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence to conduct fund management activities for institutional investors and accredited investors in Singapore. BGA and BGAS are wholly owned subsidiaries of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Europe

Scottish Mortgage Investment Trust PLC (the “Company”) is an alternative investment fund for the purpose of Directive 2011/61/EU (the “AIFM Directive”). Baillie Gifford & Co Limited is the alternative investment fund manager (“AIFM”) of the Company and has been authorised for marketing to Professional Investors in this jurisdiction.

This content is made available by Baillie Gifford Investment Management (Europe) Limited (“BGE”), which has been engaged by the AIFM to carry out promotional activities relating to the Company. BGE is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform promotional, advisory and Individual Portfolio Management activities. BGE has passported its authorisations under the mechanisms set out in the AIFM Directive.

Belgium

The Company has not been and will not be registered with the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten / Autorité des services et marchés financiers) (the FSMA) as a public foreign alternative collective investment scheme under Article 259 of the Belgian Law of 19 April 2014 on alternative collective investment institutions and their managers (the Law of 19 April 2014). The shares in the Company will be marketed in Belgium to professional investors within the meaning the Law of 19 April 2014 only. Any offering material relating to the offering has not been, and will not be, approved by the FSMA pursuant to the Belgian laws and regulations applicable to the public offering of securities. Accordingly, this offering as well as any documents and materials relating to the offering may not be advertised, offered or distributed in any other way, directly or indirectly, to any other person located and/or resident in Belgium other than to professional investors within the meaning the Law of 19 April 2014 and in circumstances which do not constitute an offer to the public pursuant to the Law of 19 April 2014. The shares offered by the Company shall not, whether directly or indirectly, be marketed, offered, sold, transferred or delivered in Belgium to any individual or legal entity other than to professional investors within the meaning the Law of 19 April 2014 or than to investors having a minimum investment of at least EUR 250,000 per investor.

Germany

The Trust has not offered or placed and will not offer or place or sell, directly or indirectly, units/shares to retail investors or semi-professional investors in Germany, i.e. investors which do not qualify as professional investors as defined in sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB) and has not distributed and will not distribute or cause to be distributed to such retail or semi-professional investor in Germany, this document or any other offering material relating to the units/shares of the Trust and that such offers, placements, sales and distributions have been and will be made in Germany only to professional investors within the meaning of sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB).

Luxembourg

Units/shares/interests of the Trust may only be offered or sold in the Grand Duchy of Luxembourg (Luxembourg) to professional investors within the meaning of Luxembourg act by the act of 12 July 2013 on alternative investment fund managers (the AIFM Act). This document does not constitute an offer, an invitation or a solicitation for any investment or subscription for the units/shares/interests of the Trust by retail investors in Luxembourg. Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units/shares/interests of the Trust to retail investors in Luxembourg.

Switzerland

The Trust has not been approved by the Swiss Financial Market Supervisory Authority (“FINMA”) for offering to non-qualified investors pursuant to Art. 120 para. 1 of the Swiss Federal Act on Collective Investment Schemes of 23 June 2006, as amended (“CISA”). Accordingly, the interests in the Trust may only be offered or advertised, and this document may only be made available, in Switzerland to qualified investors within the meaning of CISA. Investors in the Trust do not benefit from the specific investor protection provided by CISA and the supervision by the FINMA in connection with the approval for offering.

Singapore

This content has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, this content and any other content or material in connection with the offer or sale, or invitation for subscription or purchase, of the Trust may not be circulated or distributed, nor may be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor (as defined in Section 4A of the Securities and Futures Act 2001, as modified or amended from time to time (SFA)) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1), or any person pursuant to Section 275(1A), and in accordance with the conditions specified in Section 275 of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where the Trust is subscribed or purchased under Section 275 by a relevant person which is:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the securities pursuant to an offer made under Section 275 except:

(1) to an institutional investor or to a relevant person or to any person arising from an offer referred to in Section 275(1A) or Section 276(4)(c)(ii) of the SFA,

(2) where no consideration is or will be given for the transfer;

(3) where the transfer is by operation of law; or

(4) pursuant to Section 276(7) of the SFA or Regulation 37A of the Securities and Futures (Offers of Investments) (Securities and Securities-based Derivatives Contracts) Regulations 2018.