Beyond Silicon Valley: The US’s Other Innovation Hubs

Ian McGugan

- The US’s most exciting companies are increasingly spread across new innovation hubs

- Scottish Mortgage managers keep a close eye on the firms emerging from these hives of invention

- The hubs thrive on government support, academic links, talent and quality of life

Please remember that the value of an investment can fall and you may not get back the amount invested.

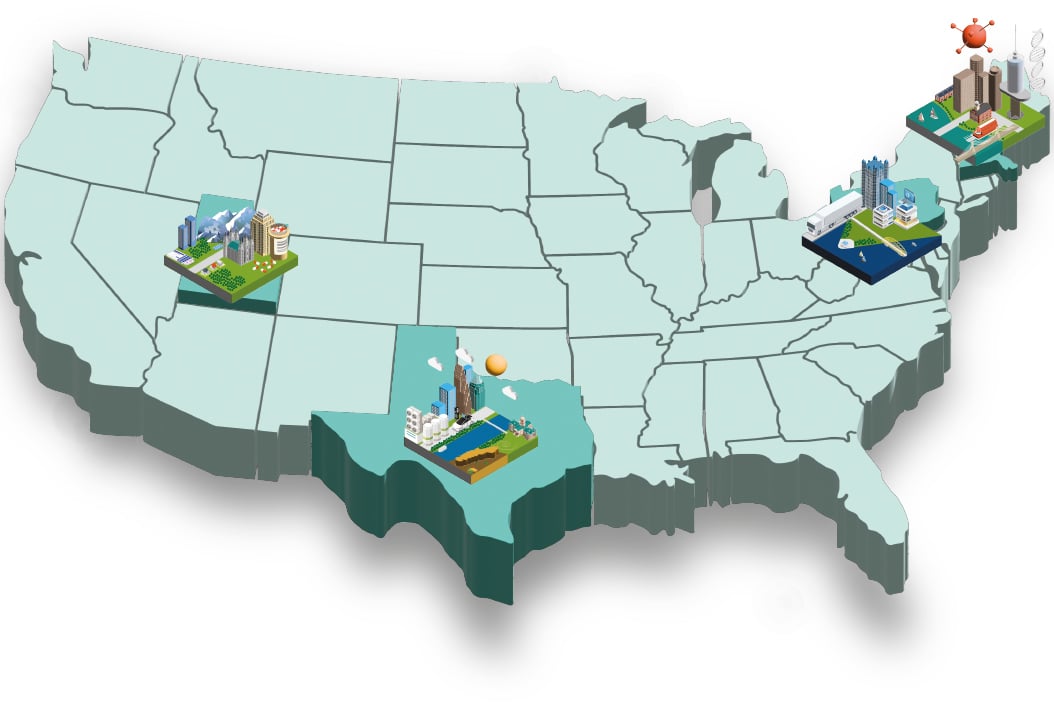

Ten years ago, Scottish Mortgage managers’ hunt for transformational companies in the US rarely took them further than Silicon Valley. Now, their research takes them far beyond California, from Boston to Houston, Pittsburgh to Salt Lake City.

“We aim to own the most ambitious and exceptional growth companies in the world, public or private,” says Claire Shaw. “As more technology clusters form across the country, these concentrations bring big benefits to Scottish Mortgage portfolio businesses.”

Over 50 per cent of the companies held by the Trust are based in the US. Increasingly, they are headquartered hundreds or even thousands of kilometres away from the historic heart of northern California’s tech industry.

What accounts for the geographic shift? Shaw cites supportive “regional ecosystems”, comprising university research centres, alert venture capitalists and appropriately skilled workers. When these factors are present, entrepreneurial ambition tends to thrive.

In some cases, the availability of pre-existing infrastructure is a powerful lure, as is federal and local government support. Texas, a designated green energy hub, is a good example.

In other cases, it’s quality of life that beckons. Many US cities look affordable compared to Silicon Valley, where the cost of a simple three-bedroom home can easily top $1.5m. Lower state taxes and proximity to the outdoors add to the appeal.

Silicon Valley remains the red-hot centre of hi-tech, Shaw acknowledges. But, as our map illustrates, the last decade has seen a blossoming of potentially world-changing businesses across the US.

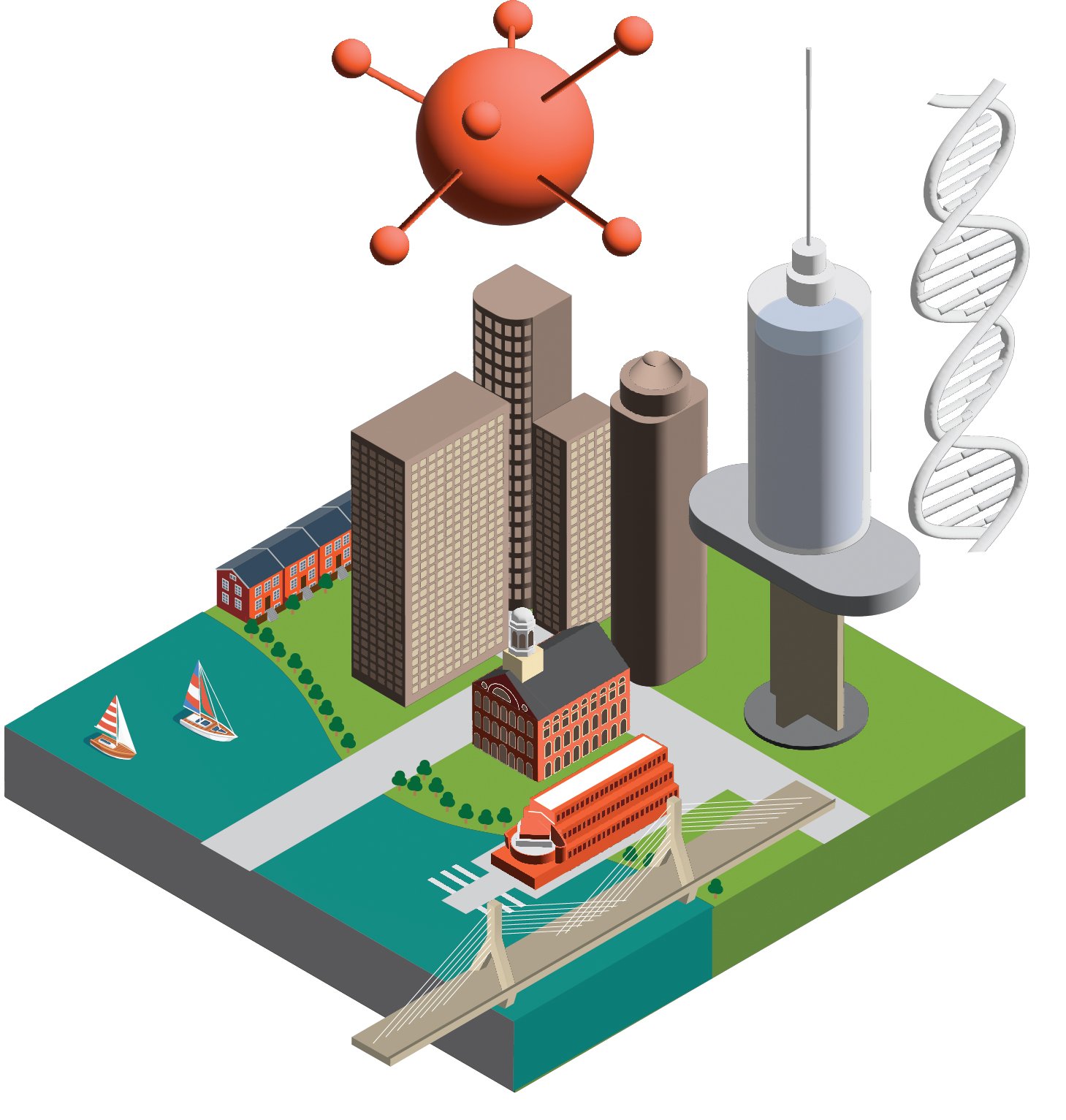

Boston’s Biotech Cluster

Massachusetts contains many of the planet’s most innovative biotechnology companies. The state has overtaken California as the global leader in biotech job growth, investment and infrastructure.

Cambridge-based Moderna, one of the Trust’s largest holdings, hit the headlines during the pandemic when its mRNA-based vaccines helped lead the fightback against Covid. Now, Moderna is repurposing the technology and using it as a platform to develop everything from better flu vaccines to personalised cancer therapies.

“It applies a Silicon Valley mentality to the drug industry,” Shaw says. “Moderna is ‘coding’ genes and proteins like software to produce drugs for flu strains and latent viruses such as herpes, and it’s pursuing a personalised cancer vaccine based on the genetic sequencing of a tumour.”

Other notable northern US innovators in the Trust’s portfolio include Insulet, a Boston-area company building insulin pumps for people with diabetes.

“Its pump can be connected to continuous glucose monitors, creating a closed-loop system almost like an artificial pancreas,” says Shaw. “Both types of diabetes are growing, which means more patients need constant monitoring of their glucose. Insulet’s pumps can be connected to the monitors and help patients’ levels stay within a safe range.”

Texas’s Climate Hub

The modern petroleum industry began in Texas in 1901, so it’s fitting that the US oil boom’s birthplace should be helping to mitigate its long-term effects. The state authorities are pushing to make it a green energy innovation hub. Tesla’s gigafactory in Austin, which opened in 2022, is a symbol of the area’s ability to attract manufacturers.

Texas is attracting some of the world’s leading companies in ‘cleantech’ thanks to strong universities, ample venture capital and highly trained energy workers whose skills are easily transferable from oil and gas.

One of the Trust’s private company holdings, Houston-based Solugen, is working to decarbonise the chemicals industry, a major CO₂ emitter. It’s replacing the fossil-fuel ‘feedstock’ found in cleaning products, fertilisers and concrete with sustainable alternatives such as corn sugar and biomass.

Climeworks, the world leader in carbon capture technology and another private holding, takes a more direct approach. The Swiss-based company recently made the state capital Austin its US base. Its technology sucks CO₂ from the air and stores it deep underground.

“It’s a negative emissions technology,” Shaw says. “It’s based on the assumption that abatement alone is not enough.” She cites the Biden administration’s $1.2bn support for a south Texas direct air capture hub, with the promise of thousands of new jobs.

Pittsburgh’s Robotics Row

A half-century ago, Pittsburgh was famed for its steel. Today, the rustbelt city has a reputation for research into self-driving technology, with a cluster of autonomous vehicle (AV) firms benefiting from the supportive environment.

Much of the credit for this transformation goes to Carnegie Mellon University. It had the foresight to start a robotics institute in 1979, when self-driving vehicles and AI chatbots were still science fiction.

Supported by local government, the university helped spawn a Pittsburgh neighbourhood dubbed Robotics Row, which is packed with AV startups and research labs.

One resident is Aurora, founded by former Uber and Tesla engineers. Its chief executive, Chris Urmson, formerly led Google’s self-driving car programme and is a Carnegie Mellon alumnus. Aurora develops software to drive trucks on highways, promising a more efficient transport network.

“The trucking industry has cult status in the US but has trouble attracting drivers in a tight labour market,” Shaw says. “It’s a really interesting company in that it’s not trying to develop the vehicles. Aurora develops the software then partners with truck companies such as Volvo and DAF Trucks’ parent, PACCAR.”

Utah’s Silicon Slopes

Salt Lake City ranked as the hottest jobs market in the United States in 2023, according to The Wall Street Journal. Utah’s booming tech sector can take much of the credit.

What makes the state so attractive? Affordable homes and access to the great outdoors help. So too do friendly business laws, tax incentives and readily available land for construction, according to the newspaper. Such selling points have helped make Salt Lake City and the next-door city of Lehi, known as Silicon Slopes, a magnet for tech companies.

Scottish Mortgage invests in Recursion Pharmaceuticals, a company aiming to use machine learning to industrialise drug discovery. “It’s running millions of miniaturised experiments based on cell analysis that would take a PhD student years and does it in a fraction of the time,” says Shaw.

Attracting talent to Utah is not a problem. Shaw recounts how Recursion’s chief executive, Christopher Gibson, described the ease of drawing workers to Utah: “He told us that if you create an incredible culture and an incredible company, you can recruit and retain people from around the world. That’s exactly what Recursion has done.”

Investments with exposure to overseas securities can be affected by changing stock market conditions and currency exchange rates. Scottish Mortgage has a significant investment in private companies. The Trust’s risk could be increased as these assets may be more difficult to sell, so changes in their price may be greater.

About the author - Ian McGugan

Ian McGugan is a business reporter for The Globe and Mail and was founding editor of MoneySense, a Canadian personal finance magazine. He lives in Toronto.

Regulatory Information

This content was produced and approved at the time stated and may not have been updated subsequently. It represents views held at the time of production and may not reflect current thinking. Read our Legal and regulatory information for further details.

A Key Information Document is available by visiting our Documents page. Any images used in this communication are for illustrative purposes only.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co and Baillie Gifford & Co Limited are authorised and regulated by the Financial Conduct Authority (FCA). The investment trusts managed by Baillie Gifford & Co Limited are listed on the London Stock Exchange and are not authorised or regulated by the FCA.

Baillie Gifford Overseas Limited (BGO) provides investment management and advisory services to non-UK clients. BGO is wholly owned by Baillie Gifford & Co. Both are authorised and regulated in the UK by the Financial Conduct Authority.

Baillie Gifford Asia (Hong Kong) Limited 柏基亞洲(香港)有限公司 (BGA) holds a Type 1 licence from the Securities and Futures Commission of Hong Kong to market and distribute Baillie Gifford’s range of collective investment schemes and closed-ended funds such as investment trusts to professional investors in Hong Kong.

Baillie Gifford Asia (Singapore) Private Limited (BGAS) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence to conduct fund management activities for institutional investors and accredited investors in Singapore. BGA and BGAS are wholly owned subsidiaries of Baillie Gifford Overseas Limited, which is wholly owned by Baillie Gifford & Co.

Scottish Mortgage Investment Trust PLC (the “Company”) is an alternative investment fund for the purpose of Directive 2011/61/EU (the “AIFM Directive”). Baillie Gifford & Co Limited is the alternative investment fund manager (“AIFM”) of the Company and has been authorised for marketing to Professional Investors in this jurisdiction.

This communication is made available by Baillie Gifford Investment Management (Europe) Limited (“BGE”), which has been engaged by the AIFM to carry out promotional activities relating to the Company. BGE is authorised by the Central Bank of Ireland as an AIFM under the AIFM Regulations and as a UCITS management company under the UCITS Regulation. BGE also has regulatory permissions to perform promotional, advisory and Individual Portfolio Management activities. BGE has passported its authorisations under the mechanisms set out in the AIFM Directive.

Australia

This information is provided to you on the basis that you are a “wholesale client” within the meaning of section 761G of the Corporations Act 2001 (Cth) (“Corporations Act”). In no circumstances should this information be made available to a “retail client” within the meaning of section 761G of the Corporations Act. This information contains general information only. It does not take into account any person’s objectives, financial situation or needs.

Belgium

The Company has not been and will not be registered with the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten / Autorité des services et marchés financiers) (the FSMA) as a public foreign alternative collective investment scheme under Article 259 of the Belgian Law of 19 April 2014 on alternative collective investment institutions and their managers (the Law of 19 April 2014). The shares in the Company will be marketed in Belgium to professional investors within the meaning the Law of 19 April 2014 only. Any offering material relating to the offering has not been, and will not be, approved by the FSMA pursuant to the Belgian laws and regulations applicable to the public offering of securities. Accordingly, this offering as well as any documents and materials relating to the offering may not be advertised, offered or distributed in any other way, directly or indirectly, to any other person located and/or resident in Belgium other than to professional investors within the meaning the Law of 19 April 2014 and in circumstances which do not constitute an offer to the public pursuant to the Law of 19 April 2014. The shares offered by the Company shall not, whether directly or indirectly, be marketed, offered, sold, transferred or delivered in Belgium to any individual or legal entity other than to professional investors within the meaning the Law of 19 April 2014 or than to investors having a minimum investment of at least EUR 250,000 per investor.

Germany

The Trust has not offered or placed and will not offer or place or sell, directly or indirectly, units/shares to retail investors or semi-professional investors in Germany, i.e. investors which do not qualify as professional investors as defined in sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB) and has not distributed and will not distribute or cause to be distributed to such retail or semi-professional investor in Germany, this document or any other offering material relating to the units/shares of the Trust and that such offers, placements, sales and distributions have been and will be made in Germany only to professional investors within the meaning of sec. 1 (19) no. 32 German Investment Code (Kapitalanlagegesetzbuch – KAGB).

Luxembourg

Units/shares/interests of the Trust may only be offered or sold in the Grand Duchy of Luxembourg (Luxembourg) to professional investors within the meaning of Luxembourg act by the act of 12 July 2013 on alternative investment fund managers (the AIFM Act). This communication does not constitute an offer, an invitation or a solicitation for any investment or subscription for the units/shares/interests of the Trust by retail investors in Luxembourg. Any person who is in possession of this document is hereby notified that no action has or will be taken that would allow a direct or indirect offering or placement of the units/shares/interests of the Trust to retail investors in Luxembourg.

Switzerland

The Trust has not been approved by the Swiss Financial Market Supervisory Authority (“FINMA”) for offering to non-qualified investors pursuant to Art. 120 para. 1 of the Swiss Federal Act on Collective Investment Schemes of 23 June 2006, as amended (“CISA”). Accordingly, the interests in the Trust may only be offered or advertised, and this document may only be made available, in Switzerland to qualified investors within the meaning of CISA. Investors in the Trust do not benefit from the specific investor protection provided by CISA and the supervision by the FINMA in connection with the approval for offering.

Singapore

This communication has not been registered as a prospectus with the Monetary Authority of Singapore. Accordingly, this communication and any other content or material in connection with the offer or sale, or invitation for subscription or purchase, of the Trust may not be circulated or distributed, nor may be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to persons in Singapore other than (i) to an institutional investor (as defined in Section 4A of the Securities and Futures Act 2001, as modified or amended from time to time (SFA)) pursuant to Section 274 of the SFA, (ii) to a relevant person (as defined in Section 275(2) of the SFA) pursuant to Section 275(1), or any person pursuant to Section 275(1A), and in accordance with the conditions specified in Section 275 of the SFA, or (iii) otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

Where the Trust is subscribed or purchased under Section 275 by a relevant person which is:

(a) a corporation (which is not an accredited investor (as defined in Section 4A of the SFA)) the sole business of which is to hold investments and the entire share capital of which is owned by one or more individuals, each of whom is an accredited investor; or

(b) a trust (where the trustee is not an accredited investor) whose sole purpose is to hold investments and each beneficiary of the trust is an individual who is an accredited investor, securities or securities-based derivatives contracts (each term as defined in Section 2(1) of the SFA) of that corporation or the beneficiaries’ rights and interest (howsoever described) in that trust shall not be transferred within six months after that corporation or that trust has acquired the securities pursuant to an offer made under Section 275 except:

(1) to an institutional investor or to a relevant person or to any person arising from an offer referred to in Section 275(1A) or Section 276(4)(c)(ii) of the SFA,

(2) where no consideration is or will be given for the transfer;

(3) where the transfer is by operation of law; or

(4) pursuant to Section 276(7) of the SFA or Regulation 37A of the Securities and Futures (Offers of Investments) (Securities and Securities-based Derivatives Contracts) Regulations 2018.